(Cuttable in NYC with its first US-based engineer. The pull from the US market is real, and Sam Kroonenburg and Ed Ring are there to win it.)

👋 Are IPO Multiples Going to the Moon? - by Taryn Pieterse

On 12 June, SpaceX listed and closed its first day above US$2 trillion, the biggest IPO on record by capital raised, north of US$75 billion. Underneath it sits an AI story. SpaceX acquired xAI earlier this year, and the book ran more than two times oversubscribed. OpenAI filed confidentially with the SEC this month, chasing a listing near US$850 billion. Anthropic closed a private round at US$965 billion before its own planned 2026 debut.

After years of frozen exits, the IPO window is open. But these three are setting the market’s mood, not pricing reality.

The Liftoff

A listing prints a number the market can model against. SpaceX is trading near 112x last year’s revenue at its first-day close, about 95x at the IPO price. NVIDIA sits at roughly 20x sales, and CoreWeave near 10x. OpenAI and Anthropic sit around 20 to 35x in private hands. The reference points exist, but they are set by rockets, compute, frontier models and a handful of breakout apps, not the median company selling AI into a finance team or a law firm. How the rest of the application layer prices is the number we still do not have.

The Gravity Problem

The median public SaaS company trades at roughly 6 to 7x revenue in 2026, down from an 18.6x peak in late 2021. If the median public comparable is single digits, that is the ceiling the acquirer or the IPO desk is modelling.

So why is venture already paying up for AI? Two bets. One, the market is bigger, because AI eats labour budgets, not just software budgets, so the revenue line can run far beyond any SaaS predecessor. Two, the multiple holds, that this revenue exits richer than pure SaaS ever did. Both could be right. Neither is proven.

How It Trickles Down

A thin exit multiple weakens the returns maths for late-stage funds, so they get disciplined at Series B and C. That flows backwards. Series A prices for a tougher next round, and seed gets squeezed on both cheque size and valuation. Public exits reprice everything beneath them.

We are seeing the opposite today. VCs are taking the bet, and AI startups are raising at around 80% above non-AI peers at Series A, per PitchBook, ballooning to nearly 4x at the latest stages. Those averages are skewed by a tiny set of supernovas that steal the headlines and pull every benchmark up with them.

So what does it mean for your next round? If the AI bets pay off, today’s prices look cheap in hindsight. If they do not, gravity wins, rounds priced on frontier-lab maths reset hard, and we may be back in a world of down rounds.

What we’re watching

At Rampersand, we back founders who know which market they are exiting into. A defensible AI product, not a thin wrapper on someone else’s model, is what we believe earns the premium instead of the median. If you are building there, we’d love to hear from you.

Released on 16 June, it ships with open weights under a permissive MIT licence and a one-million-token context window. It is a mixture-of-experts design, around 744B total parameters with roughly 40B active per token, using a DeepSeek-style sparse-attention scheme. It beats GPT-5.5 on several long-horizon coding benchmarks at about a sixth of the cost, and lands fourth on the Artificial Analysis Intelligence Index with a score of 51, the highest of any open model. Z.ai listed in Hong Kong in January and the stock is at all-time highs. Separately, Axios reported Microsoft is weighing an Azure-hosted, fine-tuned DeepSeek V4 as a cheaper engine for Copilot Cowork.

Why it matters: Frontier-adjacent capability is now downloadable, MIT-licensed and cheap, which collapses the moat for any company whose pitch rests on raw model access rather than data, distribution or workflow. The caveat: routing data through Z.ai‘s hosted API carries China data-handling risk, so the win is in self-hosting the open weights, not the API.

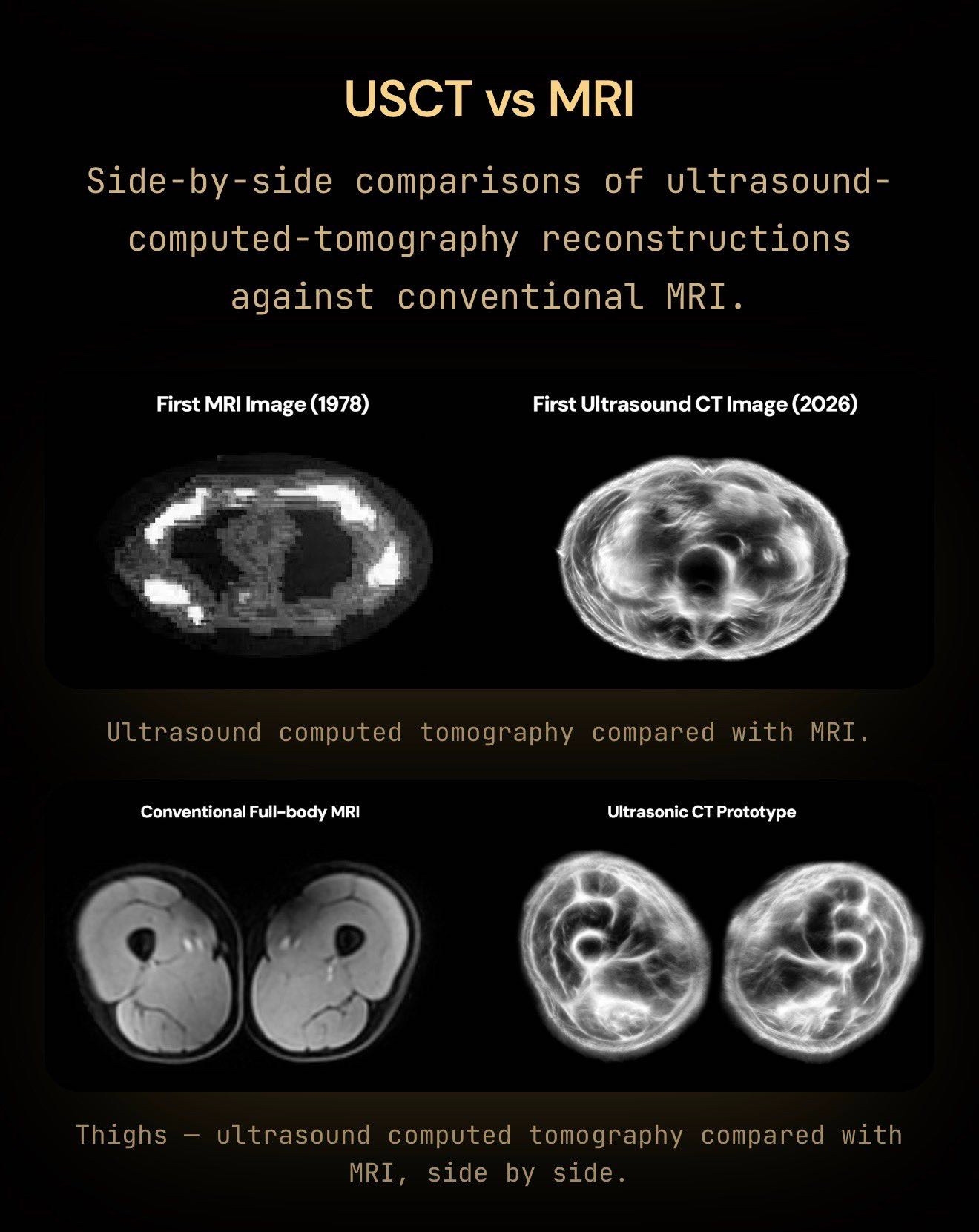

Announced on 17 June, the device is pitched as a radiation-free, magnet-free alternative to MRI. A subject stands on a platform that lowers into a shallow pool of water ringed with around half a million ultrasound sensors, built on Butterfly Network’s ultrasound-on-chip technology under a licensing deal worth up to US$74M. It reconstructs a 3D soft-tissue and bone map down to roughly half a millimetre. The current prototype takes about 20 minutes, with a 60-second goal. Midjourney, which passed US$500M in annual recurring revenue in 2025, wants 50,000 scanners running about a billion scans a month by 2031, opening its first San Francisco location in 2027.

Why it matters: A cash-generative consumer-AI company is self-funding a hardware moonshot in a regulated category, the kind of vertical, capital-efficient AI bet drawing capital in 2026. The caveat: it is a Gen-1 prototype tested on about a dozen people, with no FDA clearance and no AI in the imaging pipeline yet.

OpenAI and Polish startup Molecule.one handed GPT-5.4 a real medicinal-chemistry problem, the notoriously low-yielding Chan-Lam coupling for primary sulfonamides, and let it run the loop end to end, from reading the literature to ordering wet-lab tests. Across 10,080 reactions on an automated platform over about 2.5 months, the model surfaced a mild radical oxidant (TEMPO) as the unlock. Average yields rose from 16.6% to 25.2%, and reactions clearing 30% more than doubled. OpenAI calls it the first documented case of an AI driving an open-ended chemistry problem from literature to bench.

Why it matters: Frontier models are crossing from writing about science to doing it, which is software reaching into atoms. For founders in bio, materials and synth-chem, the moat is no longer the model, it is the proprietary wet-lab loop and the data you generate inside it. The caveat keeps it honest: humans still picked the hypotheses and validated every result.

The AI notepad that sits quietly in the background of back-to-back calls, merges your own shorthand with its transcript, and ships a structured summary the moment you hang up. It has become near-ubiquitous in VC and founder workflows since its raise earlier this year. If your team still rehydrates messy call notes by hand, this hands that hour back.

Before Cursor, Anysphere’s founders spent close to a year building mechanical-engineering and CAD tools, a stretch Michael Truell later called “wandering in the desert”. They had no domain edge, the fit was wrong, so they killed it and rebuilt around AI coding. The rule is not “have the right idea first”. It is ship something small, read the signal honestly, then double down or walk away fast. That discipline took Cursor to roughly US$2bn ARR and, on 16 June, an agreed US$60bn all-stock sale to SpaceX, the largest acquisition of a venture-backed startup on record.

Takeaway for founders: Conviction is earned by shipping and listening, not by waiting for the perfect plan. Build, measure, then commit or kill. Cursor launched 8 times on Hackernews, from AI companion to Code Editor. Take the courage.

Aircall’s first product was deliberately tiny: free, inbound calls only, a number, a greeting and opening hours. It pulled in around 100 users in about six weeks. Co-founder Jonathan Anguelov resisted charging, arguing the product was too raw, while co-founder Olivier Pailhès pushed to switch to paid. They charged. Half the free users churned on the spot. The half who stayed had a real problem and gave feedback worth acting on. As Anguelov put it, when people pay their feedback is real, whereas free users can tell you anything and you have no idea whether it matters. Aircall went on to become eFounders’ (now Hexa) first unicorn.

“Once people pay, their feedback is real. Free users can tell you anything. You have no idea if it actually matters.”

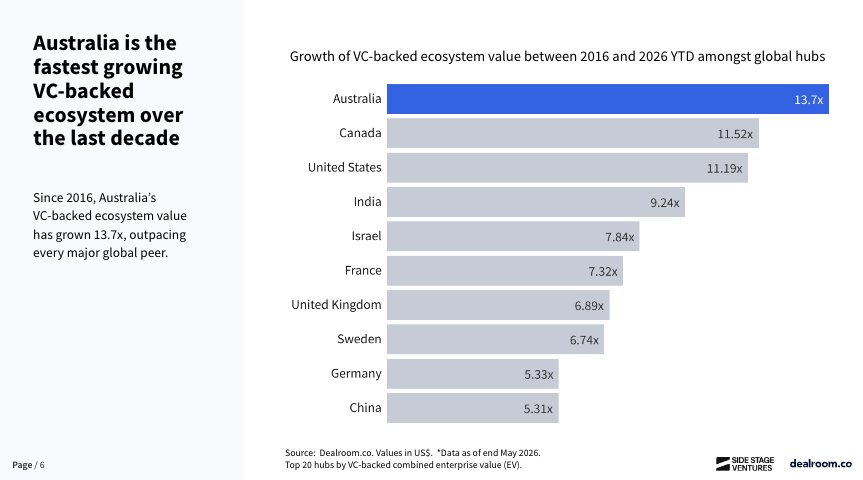

Side Stage Ventures’ new Australia Venture & Startup Report 2026, built with Dealroom, AWS, Vercel and the Australian Investment Council, benchmarks ten years of local venture against global peers. The headline: Australia’s ecosystem has grown 13.7 times faster than any other major hub, posted a 24.4% pooled five-year return (nearly double US peers), and now hosts 470-plus VC-backed AI startups worth a combined US$34.9bn, up 6.3x since 2019. The catch sits at the bottom of the funnel. Early-stage investment has fallen every year since 2021, just 18 local funds did five or more seed deals last year, and founders now raise 41% of early capital from overseas.

Why it matters: The exits and returns are world-class, but the seed engine that feeds them is thinning. For ANZ founders, raising early rounds is still a contact sport, and increasingly an offshore one.

JigSpace has signed a three-year partnership with GB Railfreight to deliver spatial-computing crew training on Apple Vision Pro. Crews explore the cab and components of GBRf’s new Class 99 locomotives in true-to-scale, interactive 360°, from anywhere in the country rather than travelling to a training school. GBRf projects the shift will save over £500,000 across two years. GBRf’s David Golding said Apple Vision Pro lets teams interact with locomotive components from anywhere with unprecedented realism.

Takeaway: Software meets atoms, made operational. JigSpace is turning heavy industrial equipment into a spatial training environment, with a hard ROI number a customer will put its name to.